We all know about the psychology of money but what about the strategy of money?

I entered this phrase into a number of search and AI tools and overwhelmingly the most prevalent results related to budgeting, spending less than you earn, automated savings/investing, debt management and retirement planning. Everything you need to know on the front-end of building your cache.

There is little publicly written on the back-end strategy of withdrawing your cache. I first wrote about strategy over a year ago. Even various searches on financial planning or retirement strategies of investments mostly resulted in generalized content from large institutions comfortably focused on building income and investments on the front-end.

What’s often not addressed are strategies for the back-end, identifying or protecting your assets for long-term health, agility, care, moving, downsizing, estate planning, philanthropy and legacy. And this brings it back to that polarizing concept of legacy. The back-end strategy of money isn’t about preparing for the end. It’s about protecting what you’ve built and preserving your ability to live the life you want for as long you can.

What does it even mean to be strategic?

At its core, being strategic means planning for the long-term, anticipating future trends and making decisions based on how they will impact overall goals rather than immediate, short-term tasks. It involves stepping away from immediate, operational or tactical tasks to consider the broader, often external, unknown context of a situation, such as potential shifts or risks.

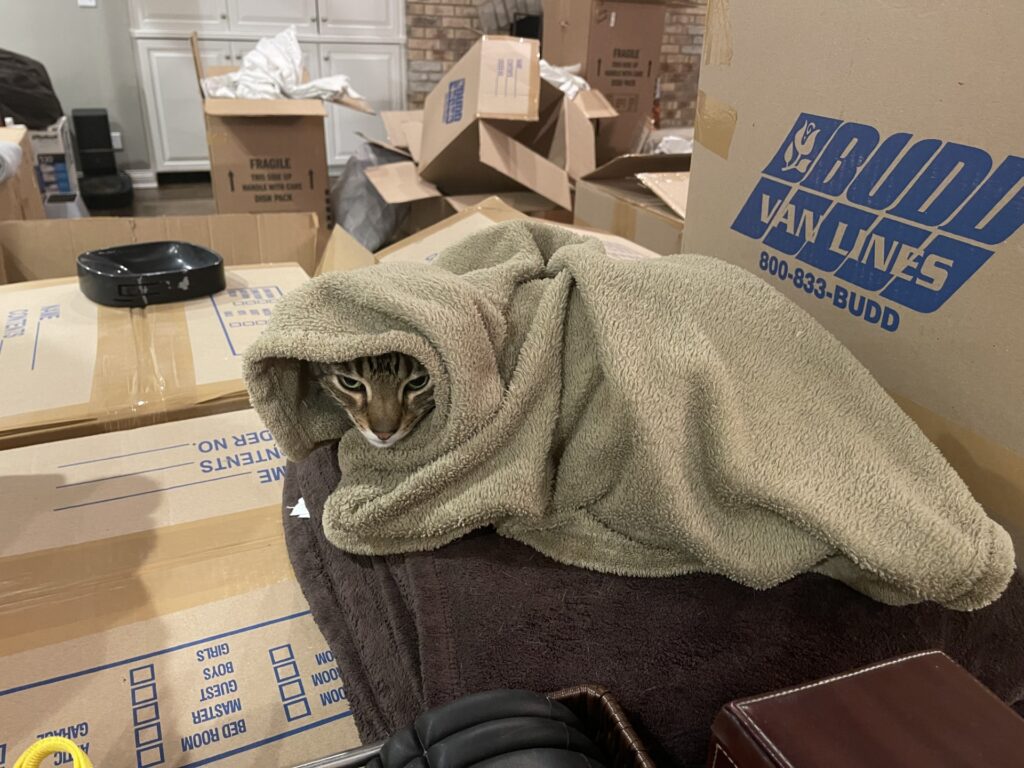

The featured image depicts the front-end strategy of moving. Everything is packaged and built up into strategic staging. There is specific packing, stacking and staging protocols that are followed to optimize the loading onto the moving truck for long haul distances. This includes identifying the critical things you need to move yourself should something happen to the truck. Or as the case when we moved to California, we packed up an entire Pod of our most critical items, and had it delivered to our temporary housing that we lived in for over a year during the housing crisis.

It takes considerable planning and strategy execution for everything to work as planned. And for all of our moves, this have been the case. You would think by the 4th one, we would be experts at this. And yet, the back-end of our last move was pretty much chaos. It was the worst unpacking experience we ever had.

The supply chain was still disrupted as a result of Covid, so the moving company didn’t have the specific packing materials to protect the fragility of dishes and other delicate items. So, the packers used a cautionary overabundance of packing paper. The labor supply was also still impacted so we had first-time inexperienced packers. Plus, no one was moving in January.

This resulted in a few items amongst the overly stuffed boxes of packing paper which led to far more boxes to unpack. It didn’t matter to the trucking company because the truck had abundant space to accommodate this. It also resulted in many other items particularly electronics being damaged due to inappropriate packing. We had never filed a claim before and this time it was over 5 figures.

It also took forever to unbox, unwrap and find everything. We had strategically identified which room each furniture piece and corresponding boxes had to be placed but it didn’t go as planned. The amount of furniture and boxes we had to move around ourselves to different floors was overwhelming especially when you are no longer in your 30’s. Fortunately, we had much more space and a big garage where we put all the broken-down boxes and flattened packing paper.

For financial planning, our front-end was detailed in numbers yet tactical in execution. With the back-end of our plan, our intent is to be much more strategic. We’ve enlisted the help of a certified financial planner and integrated tools that make information so much more accessible and in real-time.

We are on our 4th financial adviser/planner, one who can guide an appropriate strategy for our specific situation instead of a one-size-fits-all approach or ghosting us after a great introductory call. The financial modeling tool we are using is fully accessible for us to change the inputs, especially spending and what years that spending might change.

It also has fields for the ticker symbol and number of shares owned for all our other investments held with other institutions for concurrent tracking. All the investment inputs and saved spending inputs are pulled real-time modeling the numbers out to our late 90’s. It doesn’t give us only 1 modeled number at that end point in our 90’s. It gives us a significantly below average market number, a below average market number and an average market number. The goal is for all 3 to be sufficiently positive and remain so.

This allows us to consider withdrawal strategies, tax strategies, diversification strategies, consolidation strategies, income and social security strategies, health and living strategies and eventually legacy strategies.

This isn’t our “forever” home because it has far too many stairs, upkeep, insane property taxes (and snow for me). At some point, we will move again but we will have a much stronger back-end strategy to avoid the chaos. This will include hiring help to move furniture and boxes around long after the truck is unloaded and you eventually find the solid wood cat perch stashed in the outdoor cupboard.

Being strategic with money is about intention. It’s the difference between hoping things work out vs. designing and executing a strategy that works within your own personal situation.

These Retirement Planning Steps Protect the Life You Want | Kiplinger

LIMRA: Just 1 in 5 Retirees Have a Formal Written Retirement Plan